From Energy Act to IPO: Federal Energy R&D Programs Deliver Results

The next phase of America’s energy future made its Wall Street debut this spring with resounding success. Within just a few weeks, two of the country’s most promising next-generation energy companies made their entrances to the public markets through initial public offerings (IPOs) of their corporate stock. X-energy, a Maryland-based designer of high-temperature gas reactors and fuel, raised over $1 billion in what became the largest advanced nuclear IPO on record. Fervo Energy, the Houston-based pioneer of enhanced geothermal systems, followed with an upsized IPO offering that raised $2.2 billion, making it the largest-ever clean energy IPO. In an industry where billion-dollar IPOs are exceptionally rare, to see two in quick succession is a sign of strong investor demand for firm, dispatchable, carbon-free generation as rising electricity demand reshapes the American power sector.

These financing milestones were both enabled by forward-looking federal research and development (R&D). Both X-energy and Fervo are products of the Energy Act of 2020, a landmark bipartisan federal legislation that reauthorized critical Department of Energy (DOE) innovation programs like:

- The Advanced Research Projects Agency – Energy (ARPA-E): A high-risk, high-reward research agency that funds transformative energy technologies too early-stage for private investment, modeled after DARPA.

- The Advanced Reactor Demonstration Program (ARDP): A cost-sharing program that partners the Department of Energy with private developers to accelerate the construction and demonstration of advanced nuclear reactor designs – including X-energy’s Xe-100 pebble bed reactor – on an aggressive commercial timeline.

- The Frontier Observatory for Research in Geothermal Energy (FORGE): A dedicated field laboratory that gives researchers and companies like Fervo a real-world testbed to develop and refine the enhanced geothermal systems (EGS) techniques needed to unlock geothermal energy far beyond naturally occurring hotspots.

Early-stage investments from ARPA-E laid the groundwork for X-energy’s TRISO fuel in 2020. When the Department of Energy selected X-energy in 2020 as one of two ARDP awardees, the program provided up to 50% cost-sharing for a commercial-scale project. That federal partnership enabled X-energy to complete the engineering and basic design of its reactor and fuel fabrication facility, navigate licensing with the Nuclear Regulatory Commission (NRC) and recently begin construction on its TRISO-X fuel fabrication facility in Oak Ridge, Tennessee. X-energy and Dow Chemical are awaiting NRC approval of their construction permit application for the four-unit, 320-MWe Xe-100 plant at Dow’s manufacturing facility in Seadrift, Texas.

Fervo Energy’s story is similar. Founded in Houston in 2017, Fervo has transformed the next-generation geothermal industry using tools pioneered by the oil and gas sector during the shale revolution. Fervo’s technique uses applied horizontal drilling, hydraulic fracturing and fiber-optic sensing to unlock resources that were once considered too difficult or too expensive to tap at scale.

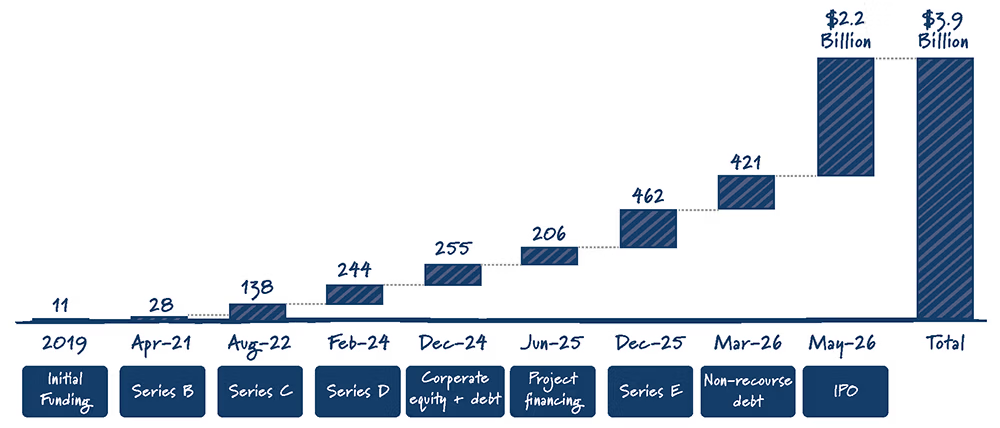

Fervo Energy’s Publicly Announced Funding to Date and Most Notable Investors

Source: Rystad Energy

Like X-energy, ARPA-E grants to Fervo Energy as early as 2019 paved the way for the company’s dynamic growth. Fervo’s founders also benefitted from DOE-aligned fellowship programs, including Activate and Cyclotron Road, a DOE lab-embedded entrepreneurship program at Lawrence Berkeley National Lab, unlocking critical expertise to validate the company’s technology at its earliest stages.

The results speak for themselves. Between 2022 and 2025, Fervo reduced drilling times by approximately 80%. The Utah FORGE site helped unlock these commercial breakthroughs, allowing the company to develop and test the stimulation and reservoir engineering techniques that now define its approach. As a result, Fervo’s flagship Cape Station project in Utah is on track to begin delivering electricity this year.

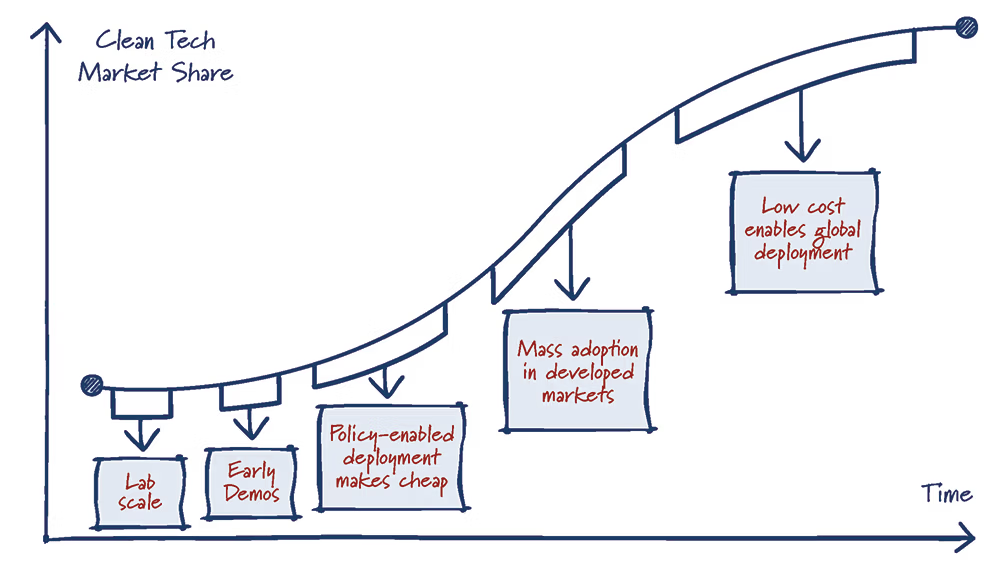

Federal R&D and Demo Funding Catalyzes Tech up the S-Curve

Today, most of the Energy Act of 2020 programs that made Fervo and X-energy’s first-of-a-kind projects possible are expiring or have already expired. As energy demand continues to grow, Congress has the opportunity to reauthorize these programs that will help America continue to lead the world in energy innovation, win the AI race and meet rising energy demand. In the six years since the Energy Act of 2020, much has changed in the energy sector and DOE needs the most up-to-date set of tools to support exciting new technologies like quantum computing, enhanced grid technologies and energy storage. These IPOs should be the green light needed to recommit to fully authorizing and funding DOE’s R&D apparatus for the AI era.

The innovation programs authorized under the Energy Act of 2020 are the engine of American energy dominance for the next generation of firm clean power technologies. Capital markets have proven the model works. Now, the conditions are right for a similar bipartisan Congressional effort to unlock the next Fervo, the next X-energy, and ensure the next energy tech unicorn has the same federal R&D foundation to build on.