Carbon Utilization 101

Carbon dioxide (CO₂) is a resource to be harnessed, from oil production and agriculture to critical minerals and advanced materials. Carbon is a fundamental building block of modern society. For decades, the United States has used carbon dioxide for energy production through enhanced oil recovery (EOR). Today, American innovators are expanding carbon’s role as a valuable domestic resource by using it to produce fuels, strengthen supply chains and create the materials that underpin our economy.

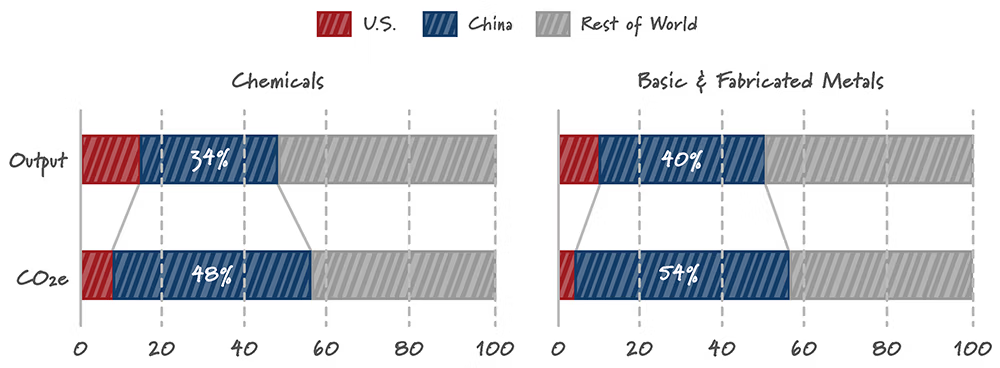

The market for products utilizing CO2 is rapidly emerging as a key part of America’s industrial and energy sectors, with global revenue projected to exceed $1 trillion by 2040. As carbon capture and removal technologies scale, increasing the supply of CO2, new utilization opportunities are emerging across the U.S. economy. Countries like China are investing in carbon capture, utilization and storage (CCUS) technologies and advancing demonstration-level projects, positioning themselves to dominate markets for products that rely on CO2 as a key input. To remain competitive, the U.S. must continue to support innovation and scale carbon utilization technologies at home, leveraging our existing capabilities to compete and lead globally.

Carbon Capture and Utilization

What is Carbon Utilization?

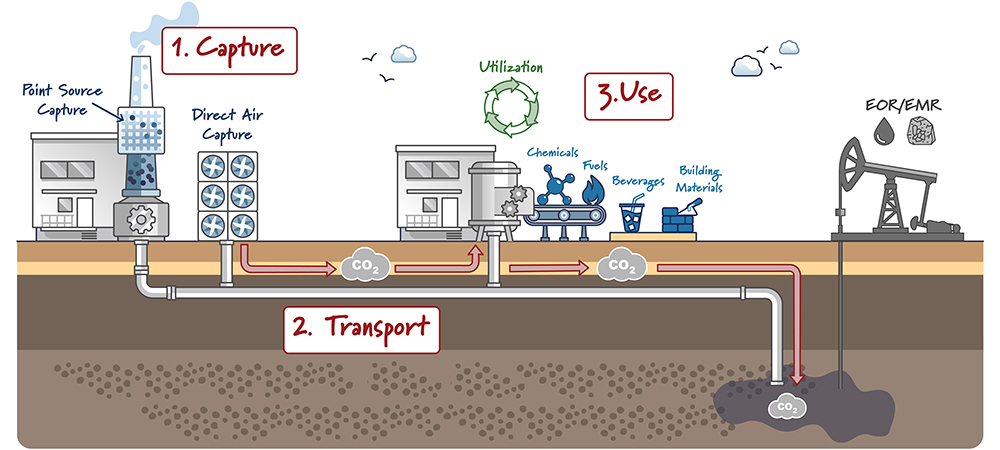

Carbon utilization, also known as carbon use or carbon conversion, refers to the use of captured CO2 from industrial sources or the atmosphere as a feedstock to produce fuels, materials, chemicals and other valuable commodities. In practice, CO₂ can serve as a building-block ingredient to create new products or as a working fluid in industrial processes that improve efficiency and unlock additional resource recovery. CO₂ can be used across a wide range of applications and sectors, supporting the production of goods that are central to the U.S. economy.

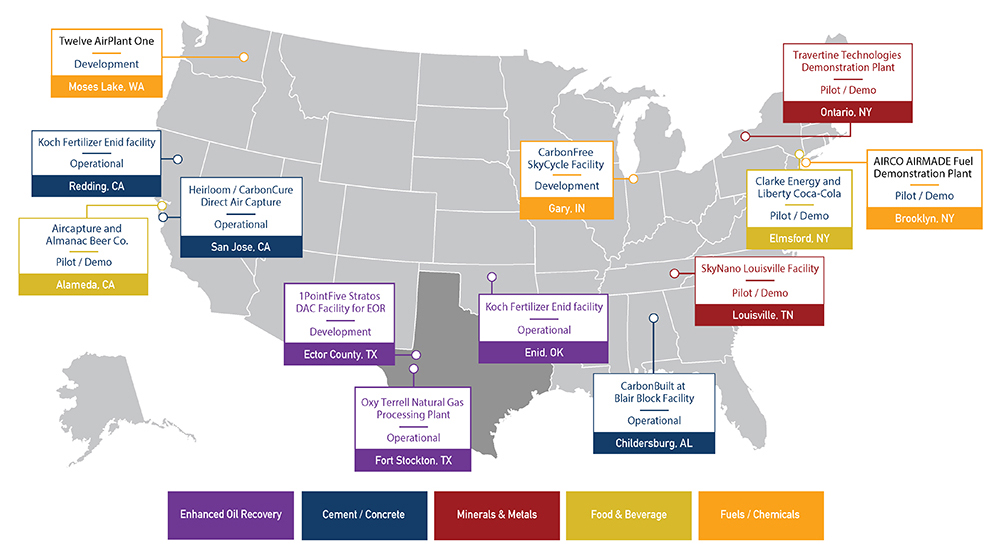

Carbon Utilization in the United States: Projects

Carbon Use Projects in the United States: Announced, In Development, and Operational

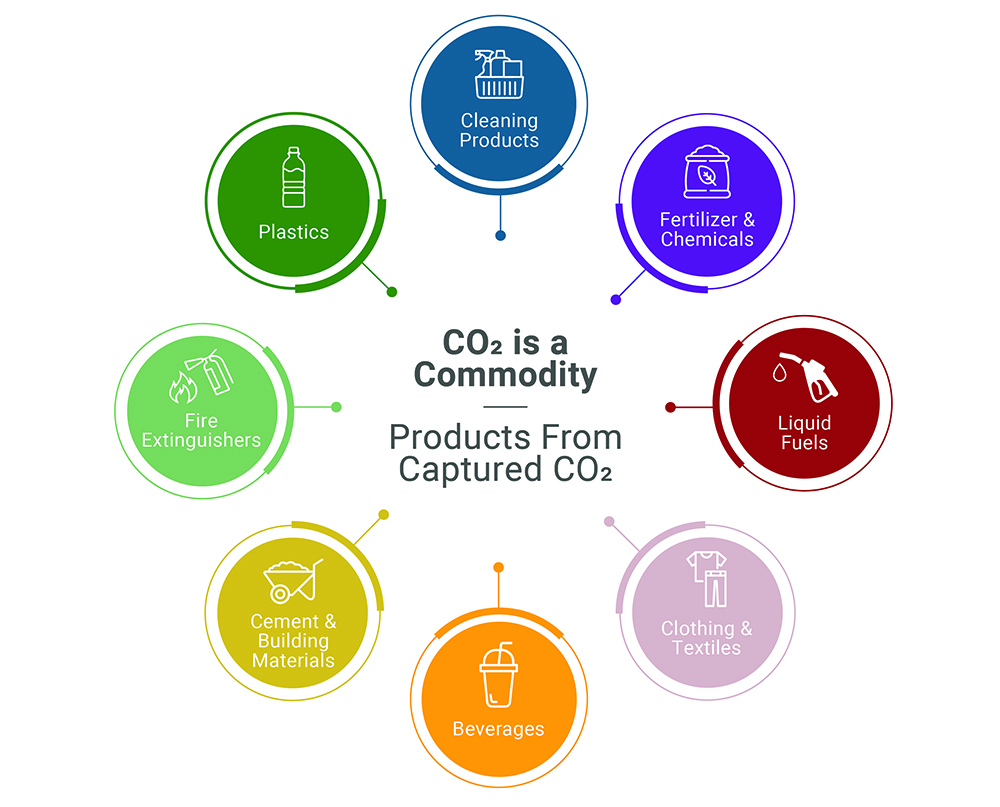

Types of Carbon Uses

American Energy Leadership: Enhanced Oil Recovery

Enhanced oil recovery using carbon dioxide (CO2 -EOR) strengthens domestic oil production, boosting energy security at home and for U.S. allies by reducing reliance on oil from adversarial nations. CO2-EOR is the most established use of captured CO2 and a key contributor to domestic oil production, enabling the recovery of 245,000 barrels of oil per day in the U.S. This process injects CO2 into mature oil fields to boost oil production and extend the life of existing assets, improving resource recovery in a cost-effective manner. During this process, much of the CO2 remains permanently stored underground, while the rest is recycled in a closed loop to support additional recovery. To make this possible, U.S operators inject approximately 68 million tons of CO2 annually for CO2-EOR.

Looking ahead, rising energy demand from reshored manufacturing, AI and data centers, combined with a growing global need for reliable American oil, will require a stable, scalable supply of domestic energy resources. Next-generation CO2-EOR technologies have the potential to unlock more than 60 billion barrels of additional oil using advanced techniques, including those that could require the injection of larger volumes of CO2. Ensuring access to a reliable supply of CO2 will be critical to sustaining and expanding this production, supporting domestic and global energy security.

Critical Mineral Independence

Similar to EOR, where CO2 can be used to bolster energy security, CO2 can also be used to extract additional critical minerals from the earth through what is often described as CO2-based mineral recovery. At ClearPath, we refer to these processes and technologies as Enhanced Mineral Recovery (EMR).

The U.S. remains 100 percent reliant on imports for 13 of the 60 minerals deemed “critical” by the U.S. Geological Survey (USGS), and EMR technologies could support domestic critical mineral production and strengthen U.S. supply chains.

EMR encompasses a range of technologies that use advanced techniques to retrieve more minerals and unlock previously inaccessible resources. These approaches can be deployed both underground (in-situ) and above ground (ex-situ) and are beginning to receive early-stage support from the Department of Energy (DOE) through programs such as ARPA-E’s MINER program.

In in-situ applications, compressed CO2, typically dissolved in water, is injected into deep rock layers where critical minerals are found. The CO2 then reacts with the minerals in the rocks to break them down and release the target minerals. While the CO2 is permanently stored underground, the leached minerals are pumped back to the surface, giving us access to additional critical minerals that were once locked underground.

In ex-situ applications, CO2 accelerates chemical reactions that extract valuable minerals or convert materials from industrial byproducts like mine tailings or steel slag into stable compounds in processing facilities, improving recovery rates. For example, CO2 can enhance the recovery of phosphoric acid, a key input for fertilizers, from phosphate, which was recently designated a U.S. critical mineral.

Agriculture Innovation

By 2050, the world will need up to 60% more food to support a growing global population, making agricultural productivity and innovation more important than ever. Agricultural innovators are leveraging captured CO2 to support controlled growing environments and develop fertilizers and other inputs that increase crop yields, improve efficiency and create new revenue opportunities.

For decades, farmers have used supplemental CO2 in greenhouses to enhance plant growth, significantly increasing plant yields. For example, by increasing CO2 levels in highly-controlled environments like greenhouses, traditionally via compressed CO2 tanks or CO2 generators, farmers can increase crop yields by 40-100%. In addition, CO₂ can be converted into chemicals for different soil amendments that provide a wide array of agricultural benefits. Specifically, CO2 is used to produce urea fertilizer, which improves soil health and nutrient retention. By utilizing CO2, farmers can strengthen the agriculture sector, enhance food security and position the United States as a global leader in agricultural innovation.

Building with Carbon

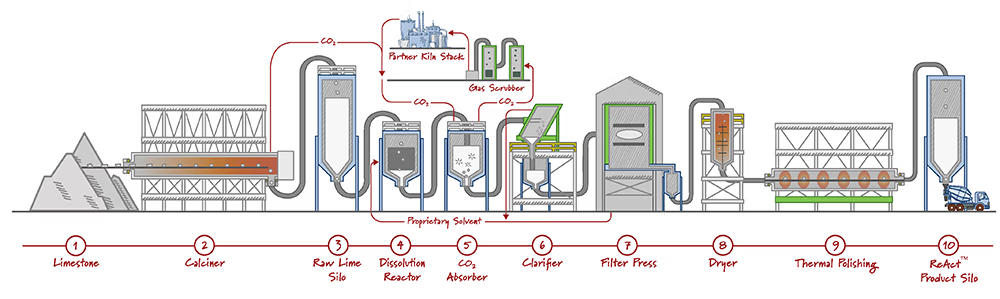

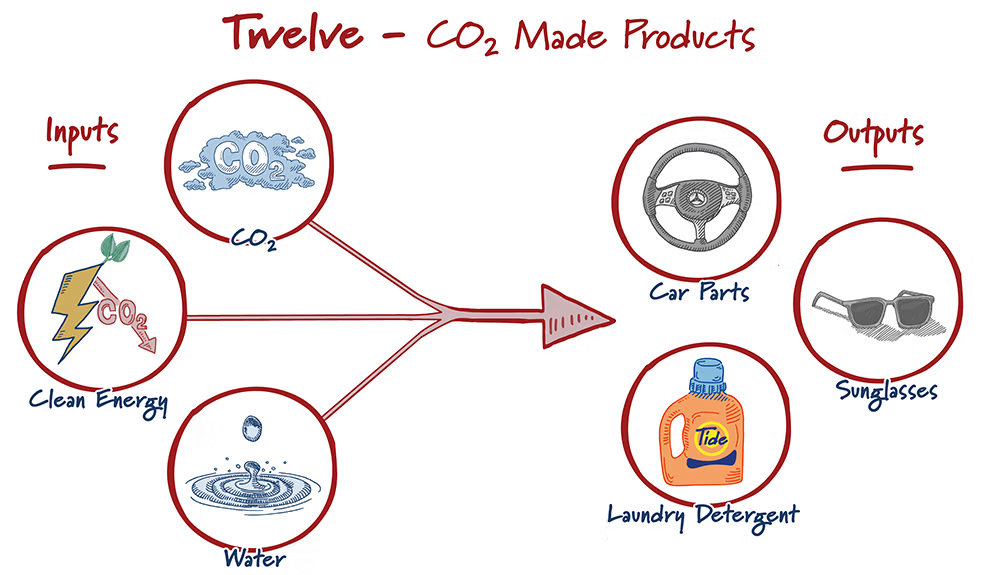

In the manufacturing sector, CO2 can be used to produce stronger, more durable materials like concrete and other industrial products, without sacrificing quality or affordability. Captured CO2 can be injected into fresh concrete, mineralized to form stable materials and permanently store the CO2, or used as a feedstock for other industrial materials. Because many of these technologies can be integrated into existing cement production facilities, they offer a pathway to rapid, scalable deployment across the construction sector.

Expanding CO2 utilization in cement and concrete can help strengthen domestic supply chains to meet growing global demand. Similarly, using CO2 as a feedstock for plastics, which exist all throughout our supply chains, can help domestic plastic production remain stable, particularly when petrochemical feedstocks are less secure. Utilizing CO2 as a feedstock creates more resilient supply chains for products we rely on, while also enhancing U.S. manufacturing competitiveness by improving product performance and enabling American-made materials to compete globally against higher-emission producers like China.

Carbon Fueling America

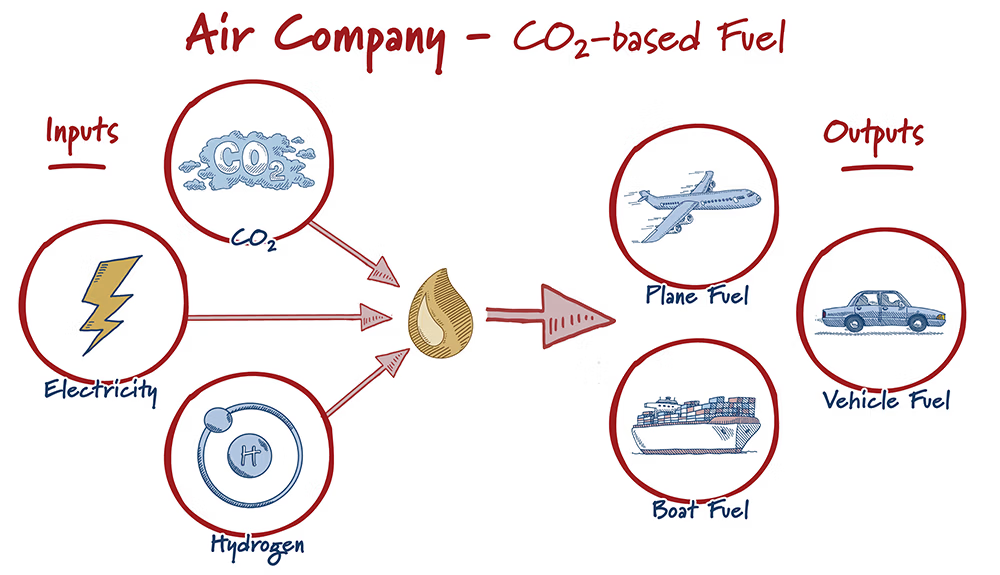

Captured CO2 can be used as a key ingredient to produce synthetic fuels and chemicals, creating new pathways to supply reliable, domestically produced energy. Innovators can convert CO₂ into liquid fuels by combining it with hydrogen or using electricity. These processes can produce sustainable aviation fuel, methanol, synthetic diesel and other fuels compatible with today’s engines and infrastructure.

Beyond commercial markets, CO2-derived fuels present a strategic opportunity for national defense. Synthetic fuels can be produced on demand in remote or high-risk environments, minimizing the risks associated with transporting fuel into contested areas and enabling greater operational flexibility for the U.S. military. The Department of War (DOW), through the Defense Innovation Unit (DIU), has supported research, development, and demonstration (RD&D) of these technologies. For example, companies have partnered with the DOW to explore and demonstrate the application of these fuel technologies across military operations.

By leveraging CO2 as a feedstock for fuel production, the U.S. can diversify its energy supply, keep production at home and strengthen our national security.

Benefits of Carbon Utilization

Carbon utilization transforms captured emissions into valuable products, unlocking new market opportunities while strengthening American energy, manufacturing and technology leadership:

- Market Opportunities for American Innovators – Today, roughly 250 million tons of CO2 are utilized annually, primarily for EOR and to produce fertilizers, but emerging technologies could more than double or triple this demand for reliable CO2 to 430-840 million tons by 2040 globally. Key markets for growth include construction aggregates and CO2-cured cement, as well as fuels made from CO2. American companies are well-positioned to lead in these emerging markets, driving innovation, creating jobs and strengthening U.S. economic competitiveness.

- U.S. Energy Security – CO2-EOR bolsters U.S. energy security by unlocking additional domestic energy resources. American oil reduces allies’ reliance on foreign suppliers, stabilizes global markets and helps meet energy needs at home and abroad. At a time when energy security is increasingly tied to national security, EOR provides a pragmatic pathway to strengthen both.

- Clean, Firm Power – Demand for clean, firm power is surging. Natural gas and coal generation paired with carbon capture will play a key role in delivering reliable, affordable, clean energy. Carbon utilization improves the economics of these carbon capture projects by creating additional revenue streams from captured CO2, particularly where storage is limited. This reduces costs and enhances project viability, supporting the scale-up of dependable, clean power.

- Affordable, Reliable and Competitive Products – Products made with captured CO2 can provide the U.S. with economic and supply chain advantages on a global scale. In some cases, such as building materials, CO2-based products are already commercially competitive, delivering improved performance and potential cost advantages. The United States is well-positioned to lead in these emerging markets by leveraging captured CO2 to produce high-value, globally competitive products while strengthening America’s manufacturing base.

Policy Recommendations

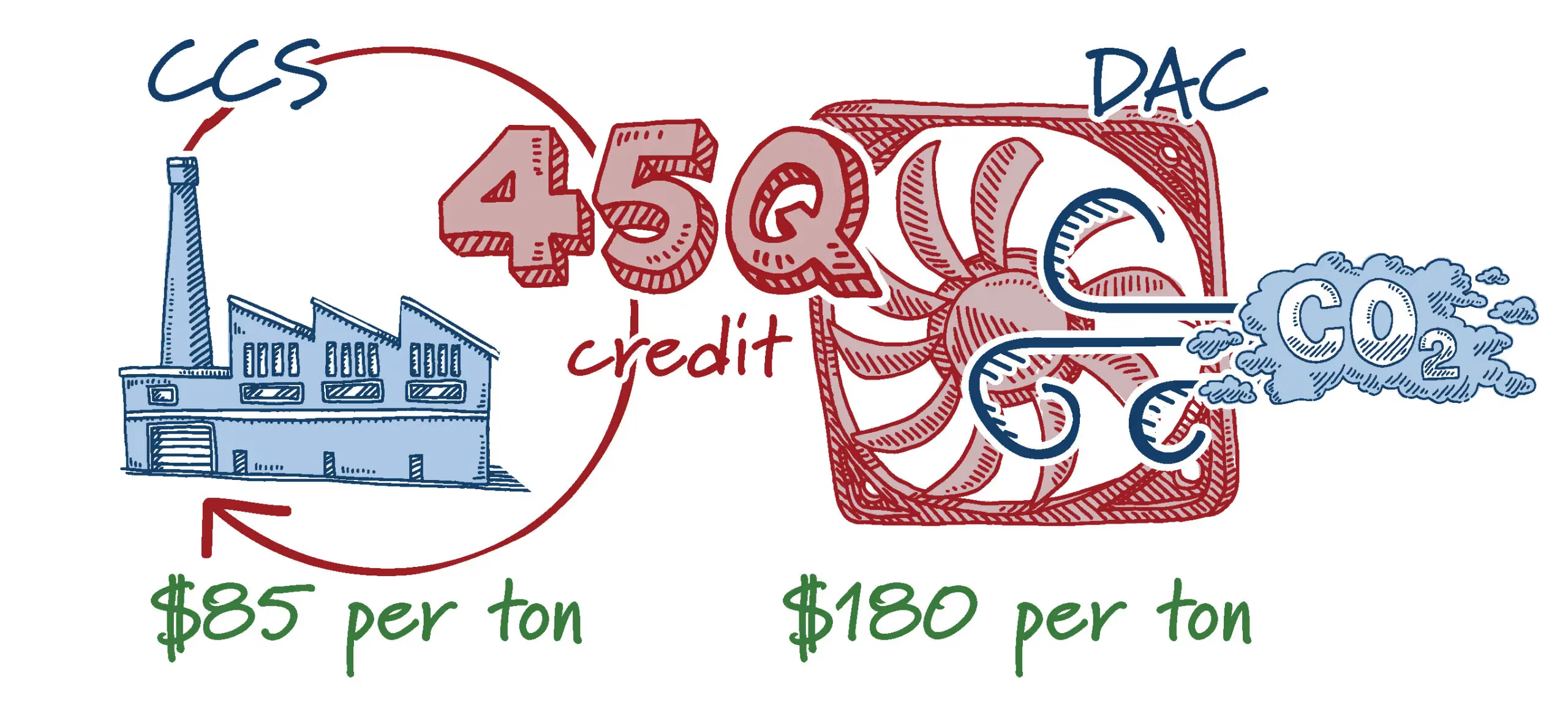

Preserve and Maintain Improvements to 45Q: The Section 45Q tax credit provides financial incentives per ton of CO2 securely utilized or stored. Recent improvements under the Working Families Tax Cuts created parity across utilization, EOR and storage — supporting technologies that turn CO2 into a valuable commodity. Preserving the improved 45Q tax credit will strengthen U.S. manufacturing competitiveness, enhance energy security and reinforce American energy leadership.

Increase the Reliable Supply of CO2: Access to consistent, high-quality CO₂ is needed to unlock the full potential of carbon utilization technologies. Investing in RD&D of carbon capture and carbon dioxide removal (CDR) technologies will help ensure a scalable, reliable supply of usable CO₂ from a diverse range of sources, including point-source capture, direct air capture and biogenic processes. Legislation supporting innovation, commercialization and deployment of these technologies, such as the Carbon Removal and Emissions Storage Technologies (CREST) Act of 2023, will accelerate cost reductions, improve efficiency, bring the most competitive technologies to market and enable broader market adoption.

Expand Carbon Utilization RD&D: Targeted federal RD&D is critical to advancing early-stage carbon utilization technologies and unlocking private investment. The Energy Act of 2020 authorized DOE”s Carbon Utilization Program, now housed within the Office of Hydrocarbons and Geothermal Energy (HGEO), to evaluate novel uses for CO₂ and demonstrate carbon utilization technologies across a range of industrial sectors. Programs like ARPA-E’s MINER initiative support research on using CO2 to unlock critical minerals, while initiatives such as the Carbon Dioxide Removal Purchase Prize help catalyze technologies that can provide and sustain a reliable, scalable supply of CO2. DOE could also coordinate with agencies such as the USGS and the U.S. Department of Agriculture (USDA) to advance cross-cutting carbon utilization opportunities across mineral, land and agricultural systems. Expanding these federal efforts will accelerate technology deployment and commercialization, broaden market opportunities and strengthen U.S. competitiveness.

Build CO₂ Pipeline Infrastructure: Expanding the nation’s CO2 pipeline network is essential to scaling carbon utilization technologies and connecting supply with demand. Projects require access to reliable, affordable CO2, which depends on a robust and well-connected pipeline system. Legislation supporting CO2 pipeline safety, R&D and streamlined interstate permitting will modernize regulations, reduce permitting bottlenecks and unlock private investment for CCUS infrastructure. This includes legislation like the PIPES Act of 2025 and the PIPELINE Safety Act of 2025, which would reauthorize the Pipeline and Hazardous Materials Safety Administration (PHMSA), as well as the Next Generation Pipelines Research and Development Act, which supports the development of advanced pipeline technologies and materials. Strengthening this infrastructure will enable more projects to move forward and reinforce U.S. energy and industrial leadership.